The Concept of Market Cycles and Its Influence on Investment Decision-Making

Investment decision-making is profoundly influenced by the patterns known as market cycles. These cycles refer to the fluctuations that occur in financial markets. Such fluctuations are primarily influenced by the factors of supply and demand, investor psychology, and broader economic indicators. Understanding these cycles allows investors to make informed decisions, optimizing their investment strategies to suit the varying conditions of the market. This adaptation is critical not only for capitalizing on profitable opportunities but also for managing risks inherent in financial investments.

Delving Deeper into Market Phases

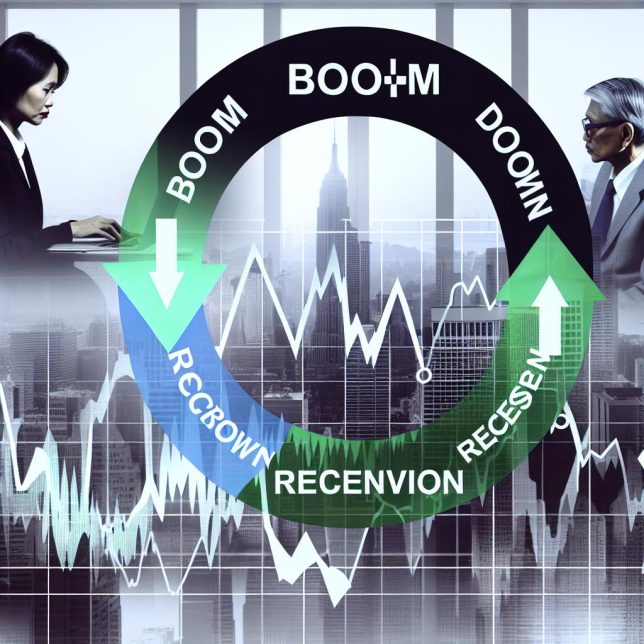

Market cycles are typically divided into four primary phases: accumulation, uptrend, distribution, and downtrend. Each phase presents distinctive characteristics and opportunities that investors can leverage, provided they are executed strategically.

Accumulation Phase: This is the phase where prices tend to be low, mainly due to the lack of substantial interest from the majority of investors. However, informed investors with a keen understanding of market trends start purchasing assets, predicting a future upswing. This phase often acts as a recovery period following a market downturn. It’s marked by the fact that many are cautious, investing in the anticipation of the turnaround. The risks are perceived to be higher as the sentiment is not broadly optimistic.

Uptrend Phase: Often referred to as a bull market, the uptrend phase is characterized by growing investor confidence, burgeoning economic growth, and a consistent rise in stock prices. During this time, the market experiences significant expansion. Demand for investment considerably overshadows the available supply, creating lucrative opportunities for investors to maximize returns. In this phase, the focus is geared toward high-performing equities and aggressive investment strategies that capitalize on the uptick. However, vigilance is crucial as this phase sets the groundwork for the subsequent stages of the market cycle.

Distribution Phase: This phase represents the market’s peak, where prices are at their zenith. Informed investors start liquidating their positions, anticipating an eventual decline. The distribution phase is noted for heightened trading volumes and increased volatility as investors begin to diversify or take profits. This period marks a critical juncture where strategic decision-making is imperative to preserve gains and mitigate potential losses. Recognizing this phase can provide investors an edge in repositioning or reallocating assets appropriately.

Downtrend Phase: Also known as a bear market, the downtrend phase is distinguished by plummeting prices, heightened selling pressure, and prevailing investor pessimism. Generally, economic indicators are weak, and the market’s atmosphere is dominated by apprehension, causing investors to pivot toward safe-haven assets. During this challenging phase, astute investors focus on preserving capital, reassessing risk appetites, and identifying opportunities for future profits when the cycle shifts back toward accumulation.

The Strategic Impact of Market Cycles on Investment Decisions

The positioning of the market within its cycle can significantly sway investment strategies and decisions, influencing how investors approach their portfolios and market engagement.

Timing: A profound understanding of market cycles enables investors to time their entry and exit positions proficiently. By purchasing during the accumulation phase and selling during the distribution phase, they can optimize return on investment by capitalizing on market peaks and troughs.

Risk Management: Deploying an awareness of market cycles, investors can better assess and manage market risks. For instance, during an uptrend phase, there may be an inclination to increase exposure to equities. Conversely, in the downtrend phase, there is often a move toward more conservative, secure assets, underpinning risk aversion and capital preservation.

Asset Allocation: Broad awareness of where the market stands in its cycle assists investors in rebalancing their portfolios to align with the prevailing phase. The strategic choice between growth and stability assets allows investors to maintain a preferable risk-return balance and adopt a dynamic approach to investment management.

Effective Tools for Analyzing Market Cycles

To adeptly analyze market cycles, investors utilize an array of diverse tools, each offering unique insights and approaches for understanding market dynamics.

Technical Analysis: This method focuses on studying historical price movements and identifying patterns that could hint at future market behaviors. Investors employ tools such as moving averages, candlestick patterns, and the Relative Strength Index (RSI) to discern the direction and strength of market phases.

Economic Indicators: Observing metrics like GDP growth rates, employment figures, inflation rates, and consumer spending provides macroeconomic insights that underpin market cycles. Such data illuminates the overall economic climate, offering predictors of where the market might be heading.

Sentiment Analysis: This approach involves gauging investor sentiment through surveys and sentiment indices. By understanding the prevailing mood of the market participants, investors can garner clues about upcoming market trends and realign strategies to either capitalize on positive sentiment or mitigate risks in the face of growing pessimism.

Conclusion

In summary, market cycles are instrumental in guiding investment decision-making processes. Their understanding and strategic application can significantly bolster an investor’s ability to navigate market volatilities. By recognizing the various phases and fine-tuning investment strategies accordingly, investors stand a better chance of enhancing their overall financial outcomes. Although no strategy entirely eliminates risks or assures success, an informed grasp of market cycles serves as an invaluable tool within an investor’s repertoire, providing the foresight to adapt and thrive in a constantly evolving financial ecosystem.

For further insights into market cycles and developing sound investment strategies, resources such as Investopedia offer comprehensive information, and consulting with financial professionals can provide personalized guidance tailored to specific investment goals and circumstances.